Corporate Bonds

April 23, 2021

What are “Corporate Bonds”?

Corporate bonds are debt issued by public or private corporations to raise capital. Investors purchasing these bonds are lenders who expect interest or ‘coupon’ payments until the bond’s maturity. These bonds usually offer a higher yield than government bonds, as they carry higher risk and are traded on secondary markets. Bond yields are the returns realized by investors on bonds. The same is calculated by dividing the annual coupon payment on a bond by its face value or par value (assuming that the investor purchased the bond at face value).

Companies issue bonds to raise capital for various purposes, including funding their operations, mergers and acquisitions, share buybacks, refinancing debt, and expansion into new markets. There are two broad ways of raising capital: by issuing equity or by raising debt. Within debt, companies have the option of either raising money by borrowing from banks/finance companies or issuing corporate bonds to investors.

Key Learning Points

- Corporate bonds are debt issued by companies with the goal of raising capital to fund their operations and growth

- The bonds are purchased by investors who expect to receive interest to compensate for the risk they carry

- Corporate bonds are issued on the primary and secondary capital market

- Bond prices have an inverse relationship with interests meaning as interest rates increase, the bond price decreases and vice versa

- Credit risk is the risk associated with the borrower (the company issuing the bonds) defaulting on their financial obligations

- Corporate bonds are rated based on their risk of default by rating agencies with AAA bonds considered the safest (issued by highly credit worthy companies)

Factors Affecting the Value of Corporate Bonds

Interest rates

Bond prices have an inverse relationship with interest rates. This means that when interest rates rise (fall), bond prices fall (rise). For example, assume that an investor purchases a bond with a par value of US$100 and maturity of 10 years. The bond offers a coupon rate (i.e. the periodic rate of interest, which is calculated on the bond’s face or par value, and paid by bond issuers to purchasers of the same) of 2%, which means that the investor who purchases the bond and holds it till maturity will get US$ 2 per year over the tenure of the bond.

Now, if interest rates rise to 3%, the bond’s price will reduce or fall as investors will find it unattractive to hold this lower-interest paying bond. On the other hand, if interest rates fall to 1%, the demand for and the price of this higher-interest paying bond will rise.

Next, turning to bond yields, the same has an inverse relationship with bond prices. Suppose the bond’s price increases to US$110, the yield on this bond will reduce to 1.8% (US$2/US$110). On the other hand, if the bond’s price falls to US$90, the yield on this bond will increase to 2.2% (US$2/US$90). It might be noted that when a bond is purchased at face value, the bond yield is the same as the coupon rate (which here is US$2).

Credit risks

Like any other debt, corporate bonds come with the risk of issuers defaulting on their commitments. Higher-risk bonds offer a higher yield. Before issuance, rating agencies such as Standard & Poor’s, Moody’s, and Fitch rate corporate bonds for their creditworthiness and riskiness.

AAA bonds are considered to be the safest and offer the lowest yields. Under the Standard & Poor’s rating system, bonds rated as AAA, AA, A, or BBB are considered investment grade. Bonds with lower ratings are referred to as “junk” bonds or “high yield” bonds.

Inflation expectations

Inflation erodes the value of bonds. That is why inflation has a direct relationship with bond yields. If the market expects high inflation, they will demand a higher yield to compensate for the risk of inflation.

Next, real yields refer to bond yields minus the rate of inflation. If a bond offers a yield of 2% and inflation is expected at 1.25%, the bond’s real yield is 0.75%.

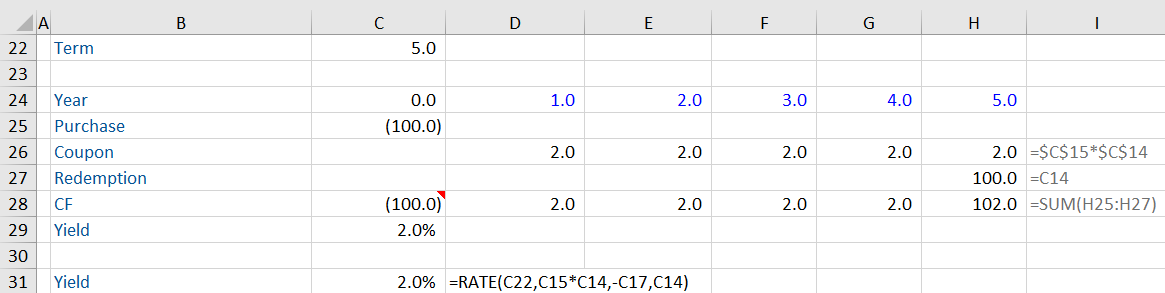

Example of bond yields

Calculate the yield of this bond based on the information below:

In this example, the bond is trading at its face value. That is why the bond yield is the same as the coupon rate.

The assumption above assumes the interest is paid in perpetuity. However, in reality, most bonds are issued for a fixed term i.e. 5 years. Let us calculate the bond yield based on this new assumption. We need to put in the term and calculate using a DCF.

The same calculation can also be completed using Excel’s RATE function.

Try downloading the workout and changing the current price of the bond to 110 based on a 5 year term. What do you notice happens to the yield?