Options

June 21, 2021

What are Options?

Options are derivative financial instruments in which two parties contractually agree to transact an asset at the strike price before or on an expiration date. The option contract gives the buyer the right, but not the obligation, to buy or sell the underlying asset. Options constitute a binding contract with strictly defined terms and properties including the strike price, options premium, and expiration date.

An option is a derivative because its price is intrinsically linked to the price of the underlying asset. In trading, context options can be purchased and traded via brokerage investment accounts. These can be used for various hedging strategies or to help generate income. In a corporate context, executive options are written by the company to their executive team. Options do not require the investor to buy or sell the underlying asset if they do not wish to. Having the obligation to buy or sell assets in the future is termed ‘futures’.

Key Learning Points

- An option is a derivative contract giving the buyer the right, but not the obligation, to buy or sell an underlying asset at the strike price on or before the expiration date.

- Options are typically classified by style into European, American, Bermudan, or by type into Call and Put options.

- A ‘Call’ option is the right to buy the underlying asset at a certain price.

- A ‘Put’ option is the right to sell the underlying asset at a certain price.

- At any given time before the expiration date an option can be ‘Out of the Money’ (OTM), ‘At the Money’ (ATM) or ‘In the Money’ (ITM).

- Options can be traded using various long or short strategies, a short position without ownership of the underlying can lead to unlimited losses.

- Options are typically used for hedging, arbitrage, to generate an income. for speculative purposes and as executive compensation.

Types of Options & Option Contracts

Options can be designed as European, American or Bermudan options, which all have different obligations. European options can only be exercised on the action expiration date, American options on any trading day on or before expiration and Bermudan options are effectively a hybrid, as they can be exercised on specified days on or before expiration.

Call Options

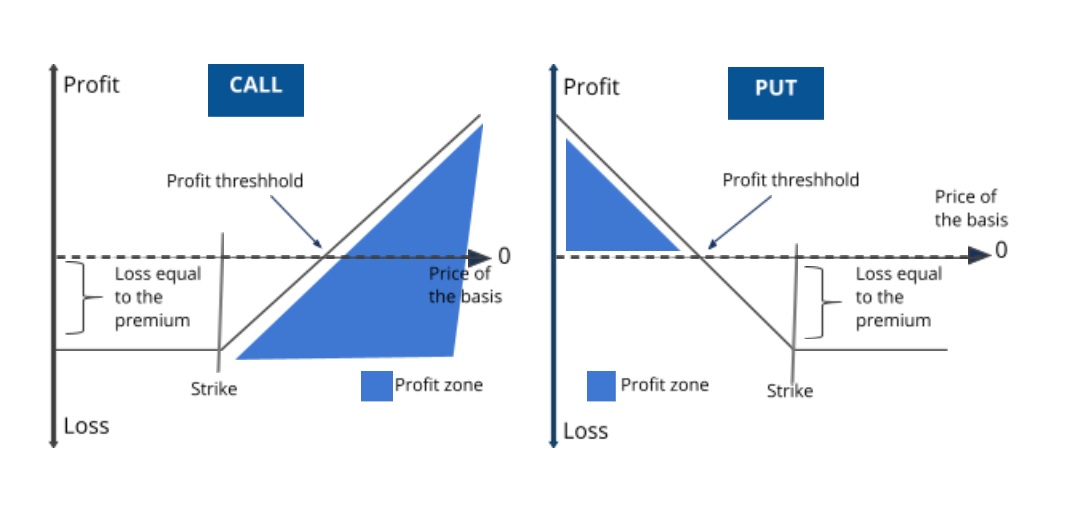

A call is an agreement that gives an investor the right, but not the obligation to buy a stock or any other security at the strike price on or before the expiration date. The risk to the call option buyer is limited to the premium paid for the option, which doesn’t include the price of the underlying asset.

Call option buyers believe the share price will rise above the strike price before the option’s expiry (hence purchasing the ‘right’ to buy it at a set price in the future). If this happens, the investor can exercise the option, buy the stock at the strike price. Subject to trading costs, they could then immediately sell the stock at the current market price for a profit. The profit on this trade is the market share price less the strike share price minus the premium and any brokerage commission to place the orders.

Put Options

A put option is an option contract giving the owner the right, but not the obligation to sell a specified amount of an underlying security at the strike price on or before expiration. The buyer believes the stock’s market price will fall below the strike price (hence buying the ‘right’ to SELL it at a set price in the future). The put option is profitable when the underlying stock’s price is below the strike price. If the prevailing market price is less than the strike price at expiry, the investor can exercise the put by selling shares at the option’s higher strike price. The profit on this trade is the strike price less the current market price, less the premium and any brokerage commission.

The chart below demonstrates the potential for profit when investing in call and put options.

At the money vs. In the Money vs. Out of the Money for Options

- If the strike price is identical to the price of the underlying security, the option is at the money (ATM).

- If the call strike price is below and a put strike price above the underlying security, the option is in the money (ITM).

- If the call strike price is above and the put strike price below the price of the underlying security, the option is out of the money (OTM).

Key Option Strategies

Long versus short, covered versus uncovered positions

With options, buying or holding a call or put option is considered a ’long’ position. Conversely, selling or writing a call or put option is a ’short’ position; the writer must sell to or buy from the long position holder or buyer of the option. Covered options are contracts sold by traders who actually own the underlying shares. In contrast, in the case of uncovered or “naked” options the writer does not own the underlying assets. Writers of naked options are unprotected and open themselves up for unlimited loss.

Long call: You buy call options, bullish strategy

Short call: You sell call options, bearish strategy

Long put: You buy put options, bearish strategy

Short put: You sell put options, bullish strategy

Example: Calculate the Options Payout for a Long Put

Please calculate the pay-off for the buyer of a three month put option in ABC Inc. The key statistics of this put are as follows:

- The put has a strike price of $3,250 and the option premium is $31.5.

- For an ITM put there is a pay-off from converting the option as the spot price lower than strike price

- For a spot price at or above the strike price, the conversion pay-off equals zero

The net profit for a range of spot prices should also consider the option premium of $31.5

Conclusion: Options Strategy Summary

The table below highlights when options may be of use to an investor depending on their view of the market, risk appetite and capacity for loss.