Cash Flow from Investing Activities Excel Workout

Sign up to access your free download and get new article notifications, exclusive offers and more.

Featured Product

Cash Flow from Investing Activities (CFI)

October 15, 2020

What is “Cash Flow from Investing Activities”?

A company lists any investments made with cash on its cash flow statement. This section represents the amount of cash used or generated from investment-related activities in a specific period.

Items reported on a cash flow statement for investing activities include purchases of long-term assets such as property, plant and equipment (PP&E), investments in marketable securities such as stocks and bonds, as well as acquisitions of other businesses.

Other items to include are a sale of a division, proceeds from the sale of PP&E, and proceeds from the sale of marketable securities and other businesses.

Some companies will have items not mentioned above, so it’s important to look at the balance sheet of a company to determine the line items.

The Coca-Cola Company – Cash Flow from Investing Activities Extract

Key Learning Products

- Cash flow from investing activities represent the amount of cash used or generated from investment-related activities (purchase of PP&E etc.)

- A positive cash flow indicates the company is divesting, a negative number indicates the company is investing heavily in its asset base to help generate growth in revenue

- The net cash flow includes the sum of all investing related activities for the accounting period

Formula

Cash Flow from Investing Activities = (Purchase)/Sale of Long-Term Assets (Capex) + (Purchase)/Sale of Other Businesses (M&A) + (Purchase)/Sale of Marketable Securities

Example

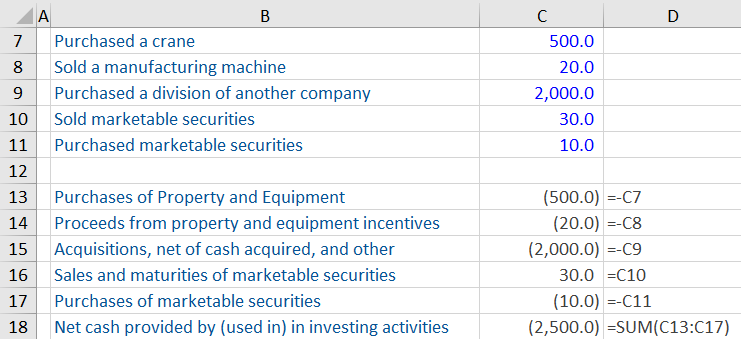

Company XYZ had the following transactions for year-ending 20X7:

The above example would reflect in the investing activities of a cash flow statement as:

Points to Note

- Purchases of the crane, a division of another company and marketable securities are an outflow of cash and must be recorded using a negative sign

- Sales of the manufacturing machine and marketable securities is an inflow of cash

What Not to Include in Investing Activities

- Debt, equity or other forms of financing

- Interest payments or dividends

- Income or expenses related to regular business operations

- Depreciation and amortization expenses on non-current assets

Why is Cash Flow from Investing Activities Important?

Although a company may report a negative cash flow in investing activities, it doesn’t necessarily mean that it’s going to have a negative impact on the business.

In the short-term, the company has faced a negative impact on cash flow due to the purchase of property, plant and equipment, but in the long-term the assets could help generate growth in a company’s revenue.

In summary, investing activities provide an insight into how effectively the company is keeping its asset base up to date, and investing for future growth.