Diluted EPS Workout

Sign up to access your free download and get new article notifications, exclusive offers and more.

Featured Product

Earnings Per Share (Diluted EPS)

October 28, 2020

What is Diluted Earnings per Share?

Diluted earnings per share or EPS shows the earnings for the period on a per-share basis as if all dilutive contracts were exercised. It uses the basic number of shares plus financial instruments that could be converted into shares. It is adjusted for convertible securities, stock options and stock units. Similar to basic EPS, the measure is designed to allow for comparison between businesses of different sizes.

Diluted EPS = Adjusted basic earnings / Fully Diluted WASO

*WASO is the weighted average shares outstanding

The calculation above looks similar to basic EPS, but there are a number of key differences. First, the earnings used for diluted EPS (those available to common or ordinary shareholders) are adjusted for convertible bond interest. The process used is called the “as if” converted method. Basic earnings are increased by the post-tax interest saved as a result of the bond converting to equity.

Key Learning Points

- Diluted EPS shows the earnings of a company on a per-share basis as if all dilutive financial contracts were exercised

- The calculation uses the weighted average shares outstanding which is the number of shares adjusted for changes across the reporting period

- Adjusted basic earnings starts at net income or earnings attributable to the shareholders of the company and adjusts for convertible bond interest

- Diluted EPS is a good indicator of profitability and is a helpful metric when comparing comparable companies

Diluted Number of Shares

The second part of the calculation is the fully diluted WASO. This starts with the basic WASO, but includes any contracts the business has which might increase the future share count. Only those which cause a decrease (dilution) of EPS are included in the calculation.

The diagram below illustrates the steps involved:

It is important to always start with the most recent filing when sourcing the basic shares outstanding. For the majority of US companies, this is found on the front page of the 10-K or 10-Q report.

Next is to adjust for the net new shares created from options using the “treasury method”. This assumes that the business will use the cash raised from the options exercised to buy back shares from the market and therefore minimize the dilution effect.

Restricted stock units (RSU) are then added. These are usually shares given to employees as compensation. These are not to be confused with “restricted shares”, which are not adjusted for since these are already issued and included in the basic share count. Out of the money options and convertible debt where conversion is unlikely are also excluded from the calculation.

Finally, for convertible bonds, the share count is adjusted by the number of new shares resulting from the exchange of bonds into equity.

Calculating Diluted EPS – Example

We are provided with the following information on want to calculate the diluted EPS:

The net income used for EPS calculations should be after any preferred dividend and after any allocation of profits to non-controlling shareholders.

To calculate diluted earnings, the net income is increased by the post-tax interest saved as a result of the convertible debt becoming equity:

The convertible debt calculation is weighted at 12/12 due to debt being in issue all year (taken from information in the table).

The impact of options to the net income is always zero because of the assumption that monies raised is used to buy back stock.

The next step is to calculate dilution from options. For this, only options which are “in the money” are considered. In the money options are defined as the holder having the right to buy the security below its current market price. Below shows the calculation for the treasury stock method:

The treasury method calculations can be summarized with the following formula:

Number of options * (Share Price – Exercise Price) / Share Price

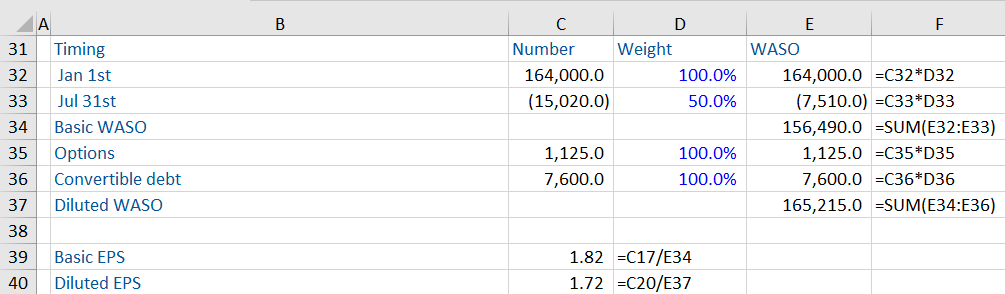

The number of shares outstanding now needs to be adjusted to calculate the basic and diluted WASO. The number of shares outstanding at the beginning of the year was 164,000. The only change to the share count during the year was a buyback that happened after six months, therefore only six months impact is included in the basic WASO.

And the basic / diluted EPS are 1.82 and 1.71 respectively: