Provisions

January 21, 2021

What are Provisions?

Provisions are funds set aside by a company to cover probable cash outflows arising in the future. If a company has a probable obligation (defined as more than 50% likely) where the payment can be estimated reliably, but it is not known for certain, then a provision is reported on the balance sheet, at the best estimate of the future payments. If the company has only a possible obligation to make a future payment, which is not probable and has less than 50% probability of occurring, then it is not shown on the balance sheet, but instead disclosed as a contingent liability in the footnotes.

Examples of provisions include tax liabilities and pension obligations. Provisions are only estimated liabilities because the exact amount to be paid out is not yet known.

Key Learning Points

- Provisions are reported on the balance sheet as liabilities as they represent a future obligation where the amount payable can be reliably estimated, but is not known for certain

- IAS 37 deals with provisions, along with contingent liabilities. Unlike provisions, contingent liabilities are only possible liabilities for the company

- There are two types of provisions: 1) Operational; which are linked to a company’s business and recurring in nature and 2) Finance; which are debt-like with a finite cash outflow in the future

- Examples provisions include lawsuits, fines, onerous contracts, tax liabilities and pension obligations.

- Finance provisions can affect the valuation of a company. When calculating the equity value, finance provisions are treated similarly to net debt. Such provisions reduce the equity value of a company

Accounting for Provisions

Provisions are recorded as an expense in the income statement and a corresponding liability is recorded in the balance sheet. Since the expense related to a provision is a non-cash expense and subjective in nature, provisions are vulnerable to accounting fraud. There is a risk that companies over-estimate the size of the provision to understate their profits in good year and vice versa, to smooth earnings growth rates.

As a result, accounting standards are designed to prevent the misuse of provisions. Under IFRS, IAS 37 deals with provisions and contingent liabilities. A provision can only be recognized when it meets the definition of a liability, which is a present obligation resulting from past events. In the context of provisions, past events can create two types of obligations:

- Legal obligations – arising from legislation or contracts,

- Constructive obligations – arising from a company’s own actions or practices and not required by the law

As mentioned earlier, a key difference between provisions and contingent liabilities is the ability to measure these liabilities. While provisions can be estimated, contingent liabilities cannot be measured reliably. Provisions are recognized on the balance sheet, but contingent liabilities are included in the footnotes only. Companies must review these items at each balance sheet date and make any changes, if necessary, to reflect any changes in estimates.

Types of Provisions

Broadly, provisions can fall into two categories:

- Operational

- Finance

Operational Provisions

Operational provisions happen in the normal course of the business. These provisions are typically linked to the company’s products or services and are recurring in nature. For example of a TV manufacturer creating provides warranties for its televisions, it is likely that small percentage of TVs will have defects, which will lead to warranty claims, and an expense for the company. The company needs to record an expense when the sale is made for the expected warranty cost, even though the defects on the TVs have not been detected yet. If a company provides a more extended warranty term than what is required by the law, it is an example of a constructive obligation.

Finance Provisions

Finance provisions have debt-like characteristics with a definite cash outflow in the future. These expenses are not created by the typical activities of the business (such as the product warranties previously mentioned). Environmental fines and lawsuits are examples of finance (or debt-like) provisions.

Finance provisions may affect the valuation of a company. When the cause of the provision is publicly disclosed, the company’s share price is likely to fall the reduction in the value of the company.

It is important to adjust for all finance provisions when valuing a company. Some provisions may have debt-like characteristics but may have been accounted for as operational provisions. Also, some provisions may not be reflected in the balance sheet (off-balance-sheet provisions). Even though they may not be shown in the balance sheet, off-balance-sheet provisions are still a liability for the company.

For valuation purposes, analysts convert off balance sheet provisions into finance provisions. This adjustment impacts the enterprise and equity value of a business. To recap from our earlier blogs, here are the formulas for equity value and enterprise value.

Enterprise value = Equity value + debt – cash and cash equivalents or

Equity value = Enterprise value – debt + cash and cash equivalents

Provisions are treated similarly to debt. If we include provisions, here is how the formulas for equity value and enterprise value look like:

Enterprise value = Equity value + provisions + debt – cash and cash equivalents

Equity value = Enterprise value – provisions – debt + cash and cash equivalents

As you can see, provisions decrease the equity value of a company. If the provisions are tax-deductible, then the post tax value of the provision should be included within these calculations.

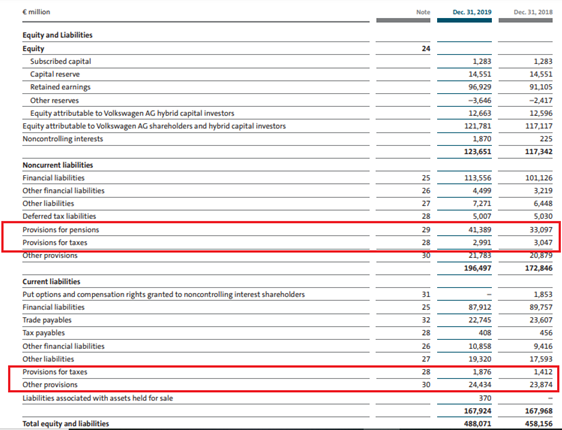

Finding Provisions in a Company’s Financial Statements

Here is an excerpt from the 2019 annual report of Volkswagen, Inc. We can see provisions listed both under noncurrent and current liabilities.

Volkswagen Group – Annual Report 2019

In the notes to financial statements, the company has included an explanation of various provisions.

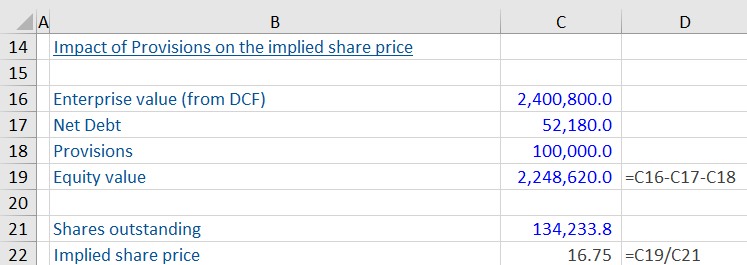

Example: Provision and Valuation

Below is the equity value and enterprise value of a company. We have been asked to calculate the implied share price, assuming provisions of 100,000 are to be treated as finance provisions.

Net debt is debt less cash and cash equivalents. As seen above, provisions will be treated similarly to net debt. This amount will be deducted from the enterprise value to get a revised equity value.

The inclusion of provisions in this calculation reduces the company’s equity value.

Consequently, this will reduce the company’s implied share price (calculated as equity value divided by the number of shares outstanding).

Additional Resouces

Allowance for Doubtful Accounts

Credit Rating

Sale and Purchase Agreement

Accounting Course