SPAC Workout

Send download link to:

Featured Product

Special Purpose Acquisition Companies (SPACs)

May 4, 2021

What is a “SPAC”?

SPAC, PIPE, DeSPACing – confused?

SPACS are Special Purpose Acquisition Companies – essentially blank cheque companies that raise funds in an IPO and then look to merge with a private operating company. Almost half of all IPOs in 2021 year to date were SPACs (source: ft.com).

SPAC issuance really took off in 2020 with 248 IPOs and $83bn raised.

Source: spacinsider.com, 2021 YTD to April 2021

Over this period the average IPO size grew by around 70% to $325m.

Key Learning Points

- SPAC IPO – the SPAC raises funds from public investors in the form of units – shares and warrants. Shares are priced generally at $10 with a warrant exercise price of $11.50. The sponsor will receive 20% of the post IPO shares outstanding. The funds are held in trust and shareholders can redeem at issue price plus any accrued interest.

- SPAC merger – The SPAC has 2 years to merge with a private operating company which effectively provides a public listing for the target company.

- PIPE investment – Private Investments in Public Companies. At the time of the merger additional shares are sold to a new group of institutional shareholders to provide balance sheet cash for the target company.

- DeSPACing – After the execution of the merger agreement, shareholders need to approve the transaction. In addition, SPAC shareholders are offered the option to redeem their shares (generally at $10). If shareholder approval is not forthcoming, then the SPAC might be liquidated unless a new merger target is

- SPACs vs traditional IPOs – Upfront fees are lower in SPACs and the operating companies merging with SPACs are able to publish 5 – 10 year of financial forecasts – a traditional IPO does not allow this.

SPAC IPO

Prospective SPAC shareholders buy into the sponsors’ experience in identifying targets and executing value add transactions. Sponsors are often private equity companies or CEOs with track records, with most SPACs being sector or geography focused. Shares are sold at $10 per share.

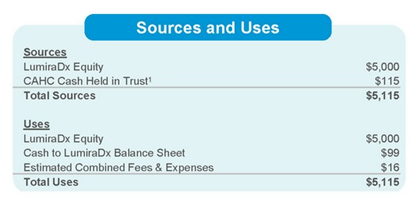

Post IPO sponsors generally hold 20% of the outstanding shares through founder shares – shares acquired at a par value. Public ownership Is through units – shares and warrants (often a fraction of a warrant). The warrant exercise price is generally set at $11.50 per share. Proceeds raised in SPAC IPOS typically represent 25 – 30% of an expected target enterprise value (see SPAC merger below). However, this relationship can drop as low as 2.5% as witnessed in the recently announced merger of CA Healthcare Acquisition Corporation and LumiraDX.

Source: https://www.sec.gov/Archives/edgar

Any funds raised will be held in trust and invested in US Treasuries until a merger with a private operating company. The cash in the trust can be used for the following:

- Redeem shares (at IPO price plus any accumulated interest)

- Acquisition of a company

- Contribute to the target company’s balance sheet – especially if the target is pre-revenue

- Distribute to shareholders if the SPAC is unsuccessful in merging with an operating company

Concurrent with the IPO, sponsors will purchase further warrants or shares, these proceeds are used to cover the IPO fees and operating expenses whilst searching for a target company. Initial IPO fees are 2% plus deferred fees of 3.5% of IPO funds raised. The deferred fees are payable upon consummation of the merger.

The SPAC will file a prospectus followed by an 8-K with an audited balance sheet post IPO.

The SPAC now has 2 years to merge with a suitable private operating company.

The model below calculates the net IPO proceeds:

SPAC Merger and DESPACing

Sponsors of the SPAC have identified a suitable target – what happens next?

Following the valuation of the private company (based on standard valuation methodologies), the negotiation of the merger agreement, and the assessment of additional funds needed (see PIPE below), the proposed transaction is put to the SPAC shareholders. Shareholders will need to approve the transaction and can redeem their shares at the original share price if they do not agree with the deal.

Target companies are often early-stage or pre-revenue companies that would find it difficult to access public markets. However, more established companies have also been merged with SPACs such as DraftKings, Virgin Galactic and PaySafe; WeWork is the latest such company.

SEC filings required are the proxy statement which will include the merger agreement, investor presentation, and other relevant documents. Following the DeSPAC transaction, SEC rules require the filing of a Super 8-K. Most of the required details will already be included in the proxy statement:

- Description of Business

- Risk Factors

- Financial Information, including:

- Three Years of Audited Financial Statements

- Selected Financial Data

- MD&A

- Quantitative and Qualitative Disclosures About Market Risk

- Director and Executive Officer Biographical Information

- Executive Compensation

- Security Ownership of 5% Owners, Directors and Executive Officers

- Transactions with Related Persons

- Material Pending Legal Proceedings

- Description of the Registrant’s Securities

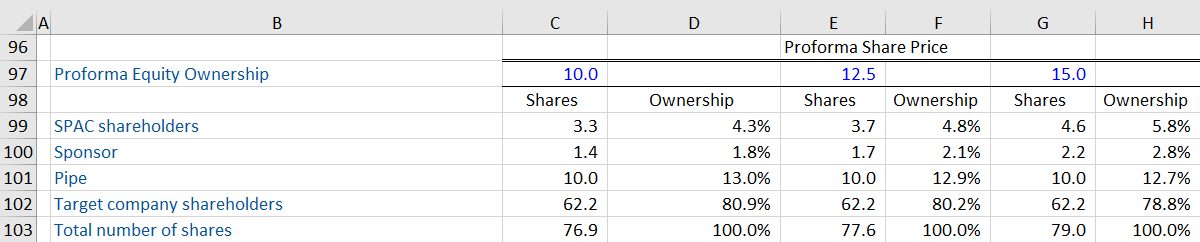

Ownership structures of the DeSPAC’d company are provided and target shareholders will now be the majority shareholders.

In our example, we have assumed that the target’s equity value is $655m.

Shares will be issued to target shareholders at $10 per share and depending on the share price post transaction, the following ownership structure will prevail. The share price will determine the exercise of warrants originally issued in the SPAC IPO.

PIPE Investment

As seen in our example above, the target company required additional balance sheet cash for operating purposes. Often the cash held in the SPAC trust is insufficient and the company issues either additional shares or debt securities in so-called PIPE transactions. The sponsor might partake or approach a new set of institutional investors who will buy additional shares at $10, the proceeds will then be used to capitalize the target company. Private Investment in Public Companies structures are not new and are conducted under Rule 144 – only qualified investors are able to participate.

The recent boom in SPACs has resulted in a large need for PIPE financing as SPACs are seeking to merge with multi-billion dollar companies and one worry is that the PIPE market is starting to dry up. According to the Financial Times (9 April 2021), only 25% of SPACs listed in 2019 have completed transactions which might be an indication that a large proportion of SPACs will have to be liquidated or extended with shareholder approval as they cannot identify or finance the acquisition of a target operation company.

SPAC vs Traditional IPO for Operating Company

A SPAC IPO is much quicker since the financial statements of a SPAC are very short compared to an operating company going public. There are no historical financial statements and business risk factors are limited. As such, SEC comments are limited and the IPO process can be completed within 8 weeks. This compares to 6 – 9 months for a traditional IPO. Upfront fees also are lower – typically the initial fees are at 2% with a deferred fee of 3.5% payable at closing of the merger. A typical IPO in the US carries underwriting fees of 5 – 7%. However, the dilutive impact of the sponsor shares (which were issued at nominal value but represent 20% of outstanding shares at the time of the IPO) and warrants should not be underestimated in assessing the true cost of SPACs.

In Summary

Source: SEC filings, FE research.

Momentus is a space transportation company that provides satellites as a service.

The company is pre-revenue. At the time of this blog, the SEC had not approved the company’s filings and a shareholder vote is needed for a 3-month extension to complete the transaction.

Look Out For…

Increased scrutiny by the SEC

John Coates, Acting Director of Corporate Finance, SEC:

“Concerns include risks from fees, conflicts, and sponsor compensation, from celebrity sponsorship and the potential for retail participation drawn by baseless hype, and the sheer amount of capital pouring into the SPACs”

Latest Updates

In recent news, shares of half of the companies that finished SPAC deals in the past two years are down 40% or more, wiping out tens of billions of dollars in startup market value! Various factors such as the threat of tighter regulations, interest rates expected to rise, and market volatility are seen to be driving their decline in performance. Discover why some investors want their money back in the WSJ’s latest article, The SPAC Ship Is Sinking.

Take Our Online Course

Take our private equity course and learn the workings of the PE industry including acquisition analysis & LBO transactions.