Amortization Workout

Send download link to:

Recommended Product

Loan Amortization

March 17, 2022

What is Loan Amortization?

Loan amortization is the splitting of a fixed-rate loan into equal payments. Each payment has an interest payment and a principal amount. More specifically, each payment pays off the required interest expense for the period, and the remaining amount goes towards reducing the principal amount.

The periodic payments in loan amortization can be easily calculated using a loan amortization calculator or table template. Lenders and borrowers can calculate the minimum payments using the loan amount, interest rate, and loan term. The common types of loans that can be amortized include auto loans, student loans, home equity loans, personal loans, and fixed-rate mortgages.

Key Learning Points

- Loan amortization refers to the process of paying off debt over time in regular installments of interest and principal sufficient to repay the loan in full by its maturity date

- Loan amortization calculations are based on the loan principal, interest rate, and the loan term

- There exists an inverse relationship between the interest payment portion and the principal payment portion of an amortized loan

- Loan amortization schedules are used by borrowers and lenders alike to a loan repayment schedule based on a specific maturity date

Understanding Loan Amortization

Loan amortization refers to the process of paying off debt through regular principal and interest payments over time. Under this repayment structure, the borrower makes equal payment amounts throughout the loan term. The first portion goes toward the interest amount, and the remainder is paid against the outstanding loan principal.

The minimum periodic repayment on a loan is determined using loan amortization. However, loan amortization does not stop the borrower from making additional payments to pay off the loan within a shorter time. Any additional amount paid over the periodic debt service often pays down the loan principal. A more significant portion of each payment goes towards the interest early in the loan time horizon. Still, a greater percentage of the payment goes towards the loan principal with each subsequent payment.

How Loan Amortization Works

Loan amortization can be calculated using modern financial calculators, online amortization calculators, or spreadsheet software packages such as Microsoft Excel. Loan amortization breaks down a loan balance into a schedule of equal repayments based on a particular loan amount, interest rate, and loan term.

The loan amortization schedule allows borrowers to view how much interest and principal they will pay with each periodic payment and the outstanding balance after each payment. It lists each period payment, how much of each goes to interest, and how much goes to the principal. The loan amortization schedule also helps borrowers calculate how much total interest they can save by making additional payments and calculating the total interest paid in a year for tax purposes.

The interest on an amortized loan is calculated on the most recent ending balance of the loan. As a result, the interest amount decreases as subsequent periodic repayments are made. As the interest portion of the amortized loan decreases, the principal portion increases because any payment in excess of the interest amount reduces the principal, reducing the balance on which the interest is calculated.

Loan amortization schedules begin with the outstanding loan balance. The monthly payments are derived by multiplying the interest rate by the outstanding loan balance and dividing by 12 for the interest payment portion. The principal amount payment is given by the total monthly payment, which is a flat amount, minus the interest payment for the month.

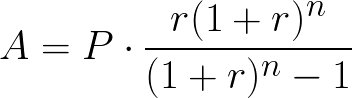

The loan amortization payment amount can be calculated using the following formula:

, where

- A: the payment amount per month

- n: the total number of periods or payments

- P: the initial principal amount

- r: the monthly interest rate

The monthly payment can also be calculated using Microsoft Excel’s “PMT” function. The user inputs the interest rate, number of payments over the life of the loan, and the principal amount.

The outstanding loan balance for the following period (month) is calculated by subtracting the recent principal payment from the previous period’s outstanding balance. The interest payment is then again calculated using the new outstanding balance. The pattern continues until all principal payments are made, and the loan balance reaches zero at the end of the loan term.

Example of a Loan Amortization Schedule

The calculations of an amortized loan can be shown on a loan amortization schedule. It lists all the scheduled payments on a loan as determined by a loan amortization calculator. The table calculates how much of each monthly payment goes to the principal and interest based on the total loan amount, interest rate, and loan term.

The simplest way to amortize a loan is to start with a template that automates all the relevant calculations. Loan amortization schedules often include the following:

- Loan details: Loan amortization calculations are based on the loan principal, interest rate, and term of the loan. When building a loan amortization table, there will be a place to enter this information.

- Payment frequency: The first column of an amortization column typically shows how frequently the repayments of a loan will be made. The most common frequency is monthly payments.

- Total payment: The total payment column represents the full monthly payment to be made by the borrower. The amounts will be automatically calculated in an amortization table template. Alternatively, the number can be calculated by hand or using a personal loan calculator.

- Extra payment: Any payment made in excess of the minimum monthly payment will automatically be applied to the principal by the amortization calculator. Future interest payments are calculated using the updated balance.

- Principal repayment: This column shows how much of each monthly payment goes towards writing off the loan principal. This number increases over the life of the loan.

- Interest costs: This column shows how much of the monthly payment goes towards the loan interest in a similar light. This number decreases over the life of the amortized loan.

- Outstanding balance: This column shows the outstanding balance on the loan after each scheduled payment. It is calculated by subtracting the principal paid each period from the current loan balance.

For instance, assume a two-year auto loan with a principal of $18 000 at a 5% interest rate. Payments on the loan are to be made monthly. The loan amortization schedule is presented below:

Based on the amortization schedule above, the borrower would be responsible for paying $789.69 per month. The monthly interest starts at $75 in the first month and progressively decreases over the life of the loan. The borrower will pay a total of $952.4 in interest over the entire loan term.

Conclusion

Loan amortization provides borrowers and lenders with an effective means of understanding how payments are applied by spreading out loan repayments into a series of fixed payments based on a specified repayment date. A portion of each periodic payment goes towards the interest costs and another towards the loan balance, ensuring that the loan is paid off at the end of the loan amortization schedule. This is particularly useful since interest payments can be deducted for tax purposes.