Cap Rates in Real Estate

February 17, 2023

What is a Cap Rate?

A cap rate, or a capitalization rate, is a metric used in real estate to measure the expected return on a property. The cap rate is a function of the value of the property relative to the operating income the property generates on a forward basis. A cap rate is reflective of the riskiness of an asset so higher cap rates imply higher risks.

Cap Rate Formula

Key Learning Points

- Cap rate is an implied return on a property based on next year or next twelve months of expected net operating income

- Cap rates reflect many factors related to the property, the local/regional market, and even the macroeconomy

- This is an unlevered return so it is critical that NOI is defined correctly (building related revenue and expenses only, maintenance capex but nothing longer term, and no financing costs)

- The inverse of a cap rate is the multiple of purchase price over earnings so a higher multiple implies a lower cap rate

- While widely used, cap rate has its drawbacks; namely, that it is based only on one year of earnings, ignores larger capex issues, and penalizes buildings with vacancy rates even though that can benefit owners who are buying into developing markets

Defining Cap Rate

While the formula for a building’s cap rate is simple, there are many factors that impact a cap rate that must be understood before using the rate in real estate analysis. First of all, a cap rate is immediately impacted by the quality of a building. Higher-quality buildings, sometimes graded by class (A,B,C, etc) attract higher-quality tenants and those leases are more valuable. These buildings tend to have high demand and fewer vacancies. Fewer vacancies and higher rents are a good recipe for a very low cap rate. Beyond the building quality and leases, building values can be impacted by their proximity to airports, public transportation, parking lots, good neighborhoods, freeways, etc. They can benefit from good housing stock or affordable housing and good schools. Local or regional growth can impact building values as neighborhoods and areas develop or grow.

Macro issues can impact buildings immensely. Certain areas of the country and certain kinds of buildings will be impacted by macro events differently than others. Rising interest rates can impact overall investment in real estate. Cap rates will likely rise with rates as investors seek returns commensurate with the market. Financing might become an issue with higher rates and access to capital but this is one macro event that would impact almost all real estate at the same time. Drops in GDP or inflation can also push cap rates up as the risk of investment properties rises.

Cap Rates and Multiples

Going back to our example above of a high-quality building with high-value leases, we would expect this building to have a very low cap rate. This low cap rate implies that there is very little risk to owning this building as the asset quality is high and lease values are high as well. Of course, the flip side of this is that those buildings will fetch high prices. This demonstrates the inverse relationship between the cap rate and the value of a building. When asset prices increase, the NOI as a percentage of the building value decreases. But if we look at that relationship inversely, the multiple of the building value over the NOI increases. So low cap rates imply paying a high multiple to acquire that asset.

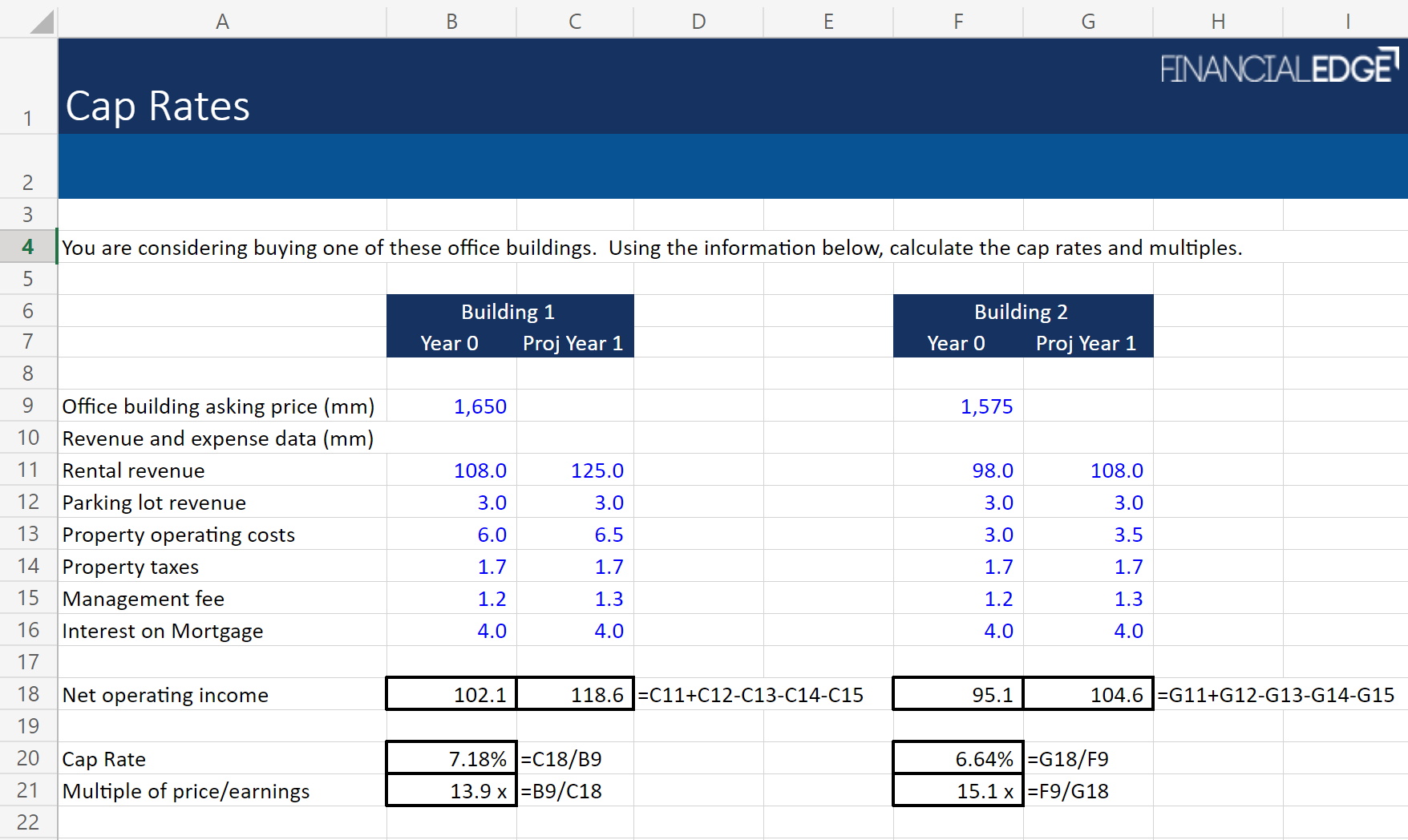

Cap Rate Calculation

In the example below, we can see the cap rate calculation (along with the corresponding multiple calc). We can also see how cap rate can be used to compare the two buildings to determine that Building 1, while on paper seems to cost more, has the potential to generate more income in the first full year of ownership (projected year 1) and so that makes it a relative value and less expensive overall. Access the free download to practice these calculations yourself.

Cap Rate Limitations

While cap rates can be a great back-of-the-envelope metric for comparing properties, there are some limitations. First of all, a successful real estate investment has several elements. One of those elements is the financing structure. Deals that are smartly capitalized can do better than other deals where the financing was not well structured. This may go for many other ventures as well but it is particularly important in real estate. Cap rate is unlevered so it ignores this element. It also ignores the other components of cost which go into running a building namely leasing fees to brokers, tenant improvements, and longer-term CapEx. Those can seriously impact returns. Lastly, it is very myopic in looking at only one year forward NOI. This undervalues buildings that have a strong five or ten-year horizon such as up-and-coming areas. It also overvalues buildings with currently high lease values but might be risky longer term. For a detailed analysis, an IRR over a projected hold period is still probably advisable.

Conclusion

Cap rates represent the expected return on investment and as such a measure of the risk/return profile. They are widely quoted and one must understand them to be in real estate. However, they do have limitations and can be misleading if a deeper analysis has not been completed.

As well as cap rates, explore other common metrics in real estate investing, and the technical skills needed for real estate financing with the Real Estate Analyst. The online real estate financial modeling course will also teach you how to get to grips with real estate modeling and valuation.