Earnings Before Interest and Taxes (EBIT)

November 9, 2020

What is “EBIT”?

EBIT is the abbreviation of “Earnings before Interest and Tax” and is a very useful calculation for measuring a company’s performance. For many companies, EBIT can simply be their operating profit which can be found on the income statement. EBIT shows how profitable the company is from its operations and does not include expenses related to taxes and capital structure, such as interest and tax expenses. Often EBIT will not equal the operating profit. This is due to the company incurring expenses that are not part of their recurring operations. Therefore they will be added back to complete the EBIT calculation.

EBIT Formula

EBIT = Operating Profit + Non-recurring + Non-core + Non-controlled

This formula assumes that items which reduce reported operating profit are positive and items which increased the operating profit are negative. It is imperative that +/- signs are correct so you don’t accidentally add an item twice!

With this formula, the starting point is operating profit (found on the income statement). We start at this figure as we are only interested in the earnings before interest or tax, as these are fixed and not relevant when forecasting. Sometimes companies do not report operating profit. In this case, you will need to start from the reported net income figure and add back interest and tax. But, this will only provide you with operating income which may not be the same as the final EBIT figure that analysts are interested in. We need to consider any further adjustments which can be made to the operating profit figure.

Key Learning Points

- EBIT is the abbreviation for earnings before interest and taxes and is a calculated number which shows a company’s recurring profit from its operations

- For some companies, EBIT is equal to their operating profit

- If operating profit is not reported, it can be calculated starting from revenues or net income

- EBIT is a popular performance tool to aid comparisons between similar companies

- The metric helps understand the recurring profit generated from operations which is useful for forecasting data

Further Steps Needed to Calculate EBIT

How is EBIT Calculated?

EBIT is calculated by subtracting a company’s cost of goods sold (COGS) and its operating expenses from its revenue. EBIT can also be calculated as operating revenue and non-operating income, less operating expenses.

As mentioned at the beginning, sometimes the operating profit of a company needs adjustments to arrive at EBIT. When stakeholders calculate EBIT, they are only interested in the earnings of the company which relates to its operations. Sometimes a company may incur an expense which is not part of its normal business but is still included in expenses, such as restructuring charges or impairments. This means that in order to calculate only the earnings generated from the business operations, any one-off expenses need to be added back on (one-off incomes or gains are deducted). Below is the order of steps you should complete to arrive at the EBIT figure:

- Start at operating profit in the income statement (if not reported then calculate starting at revenues or net income)

- Check above operating profit for any reported items which should not be included

- Check below operating profit for any reported items which need to be added back

- Check MD&A and financial footnotes for more detail and embedded non-recurring items. Use the lines above operating profit to guide your search, and use lines below operating profit as those you can safely ignore

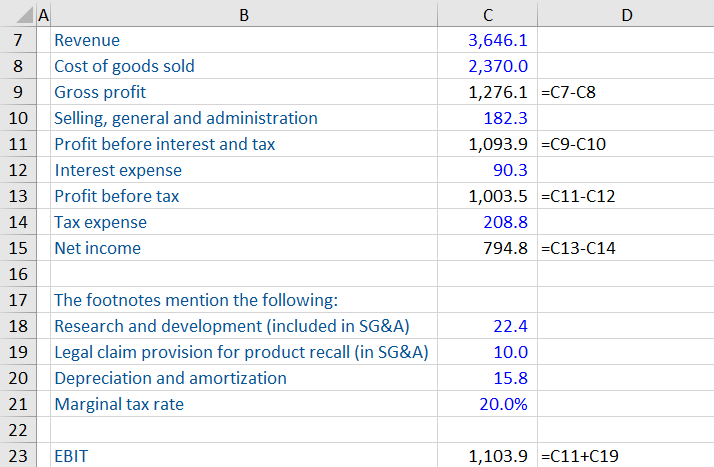

EBIT Calculation

Use the following income statement and footnotes to calculate EBIT.

The calculation starts at profit before interest and tax (operating profit) and adds back the legal claim provision included in SG&A (non-recurring item).

Bonus: To calculate EBITDA, you would need to add back the depreciation and amortization expense in cell C20.

Make sure to download the worksheet to try a bonus workout with a full solution provided.

What One-off Items Need to be Adjusted?

- Non-recurring expenses might include litigation, a one-off expense that has reduced the operating profit for the financial period.

- Non-core expenses could arise from the sale of a subsidiary, such as a gain on sale and costs directly associated with the sale.

- Non-controlled income is a result of ownership in another company (less than 50%). As this line item represents share of net income, it cannot be added to EBIT which is before interest and tax.

Why is EBIT a Popular Metric for Analysis?

EBIT is a great tool to use as a performance indicator for a company. Stakeholders want to calculate the earnings a company generates from its operations. By looking at this, an investor can see how well run the company is (are costs too high? are profit margins relative to the sector?). Investors are interested in recurring financials which can be forecasted. It is also relatively easy to calculate which makes it a great metric when comparing different companies.