Basic Shares Outstanding

March 23, 2021

What are Basic Shares Outstanding?

Basic shares outstanding are a company’s total number of shares available for trading in the stock market. It is the number of shares that have been authorized and issued to investors, which can be both institutions and individuals.

It is important to always start with the company’s most recent filing when sourcing the basic shares outstanding. For the majority of US companies, this information is found on the front page of their 10-K or 10-Q reports. If this is not available, then the outstanding shares can be calculated as:

Outstanding shares = Issued shares – Treasury shares

Issued shares are the number of shares issued by a company or the total number of shares in existence. Treasury shares are shares that had been issued but later bought back by the company as part of any share repurchases. The number of treasury shares held by companies is reported in the treasury stock account.

Key Learning Points

- Basic shares outstanding are the total number of shares issued by a company to investors. This is the number of shares available for trading in the secondary market

- Basic shares outstanding is the starting point for calculating diluted shares outstanding. Diluted shares outstanding is calculated as basic shares outstanding plus any new shares to be added due to the exercising of dilutive contracts, such as convertible securities or employee stock options

- The number of basic shares outstanding is reported in a company’s most recent filings. For any valuation assignments, it is crucial that the analyst use the most recent information available.

- The weighted average share count for the period is used in the calculation of basic earnings per share (basic EPS) which shows the earnings of a company for the period on a per share basis

- Any issuances and repurchases of common shares by the company will impact the basic shares number. However, the issue of preference shares has no impact on this number

- Equity value is calculated by multiplying the traded share price by the diluted number of share outstanding. The basic share count is not used as the share price already factors in the potential dilutive effect of dilutive contracts

Basic Shares Outstanding Vs. Diluted Shares Outstanding

Diluted shares include the effect of contracts or products the company has issued, which could result in new shares being issued in the future. The basic shares outstanding is the starting point when calculating the diluted shares outstanding. This is calculated as the basic shares outstanding plus any net new shares added as if all dilutive contracts were exercised. Examples of dilutive contracts include stock convertible securities, employee stock options and restricted stock units (RSUs).

Finding Basic Shares Outstanding in Financial Statements

Basic shares outstanding can be sourced from multiple places in a company’s financial statements. Below lists two commons sources starting with the preferred source if available.

Front Page of the Most Recent Filing

The most up-to-date number of basic shares outstanding can be found in the latest form 10-K or 10-Q of a company. The information is available on the front page of these financial reports.

Below is a snapshot from the annual report (Form 10-K) of Activision Blizzard, Inc. for 2018.

Activision Blizzard has reported the number of basic shares outstanding on the front page of its form 10-K.

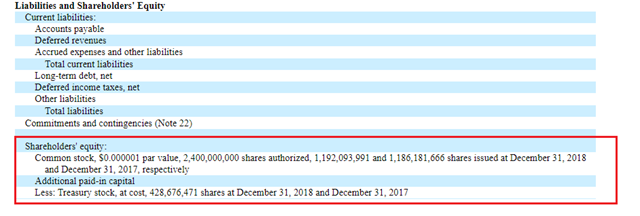

Balance Sheet

The number of shares outstanding can also be found in a company’s balance sheet in the liabilities and shareholder’s equity section.

Activision Blizzard, Inc. – Form 10-K, 2018

The number of shares outstanding in the balance sheet is as of the balance sheet date (December 31, 2018, in the example above). At this date, the company had 2.4 billion shares authorized and issued around 1.19 billion shares. The number of basic shares outstanding is calculated as the number of shares issued (1,192,093,991) less treasury stock (428,676,471). This works out to 763,417,520 basic shares outstanding.

Tip: The number of shares outstanding in the balance sheet might be out of date depending on the filing date. You should always look to the most recent filing for the updated number.

In the example above, the number of shares outstanding has increased since the balance sheet date. Note that the latest information on the number of shares outstanding is nearly 2 months after the balance sheet date.

Calculating Basic Shares Outstanding

Below is some information about shares-related transactions of a company. We have been asked to show how the following transactions will impact the company’s balance sheet and calculate the number of shares outstanding.

Issue of Equity Shares

The shareholders authorized the board to be able to issue up to 2,000 shares, of which 1,000 shares are issued at a price of 10 with a par value of 2:

The company has issued ordinary stock to raise capital. The cash balance increases by 10,000 (1,000 shares * 10 issue price). The equity accounts reflect an increase in common stock of 2,000 (1,000 shares * 2.0 par value) and 8,000 as additional paid in capital.

Share Repurchase

100 shares are repurchased at a price of 15.

The company paid cash in order to repurchase shares. The cash balance reduces by 1,500 (100 shares * 15 repurchase price). The treasury stock account under equity accounts goes down by the same amount.

Issue of Preference Shares

200 preference shares are issued with a par value of 20.

The company has issued preference shares as an alternative approach to raise capital. The cash balance increases by 4,000 (200 shares * 20 issue price). The equity accounts reflect an increase in preference shares of 4,000. However, this transaction has no effect on the company’s common stock account.

Payment of Dividend on Preference Shares

A 10% dividend is announced and paid on the preference shares.

The company has announced a dividend of 400 (4,000 * 10%) for its preference shareholders. The cash balance reduces by 400. Under equity accounts, retained earnings are reduced by a similar amount.

Overall, here is the impact of these transactions on the number of basic shares outstanding:

Only two transactions affect the basic shares outstanding count. The issue of preference shares or dividends announced to preference shareholders have no effect on this number.

Weighted Average Shares Outstanding (WASO)

The weighted average shares outstanding or WASO adjusts for the impact of any share issues or repurchases during the year. WASO is used to calculate the Similar to the calculation of diluted shares outstanding, basic shares outstanding is the starting point for calculating the WASO. This figure is then adjusted for any shares issued or repurchased during the year, adjusted for timing. If shares have been issued halfway through the financial year, then only a 6 months impact is included in the weighted average share count. We can understand this better with a simple example.

WASO Calculation

Based on the information below, calculate the weighted average shares outstanding and the basic EPS.

First, we calculate the earnings available to ordinary shareholders.

In this case, the preferred stock dividend must be deducted to get the net income used for the basic EPS calculation. The notes state that the preferred stock dividend is treated as equity, so we have removed this in the adjusted earnings calculation.

Above, the weightings have also been calculated and added to the basic shares number to calculate the WASO.

The company has repurchased 15,020 shares on June 30th. This means the shares were outstanding only for the first 6 months of the year. As a result, they have been assigned 50% weightage (6/12) when calculating the WASO. The basic WASO works out to 156,490.

The basic EPS can now be calculated as 1.77.