Operating Working Capital Excel Template

Sign up to access your free download and get new article notifications, exclusive offers and more.

Featured Course

Operating Working Capital (OWC)

February 15, 2024

What is Operating Working Capital?

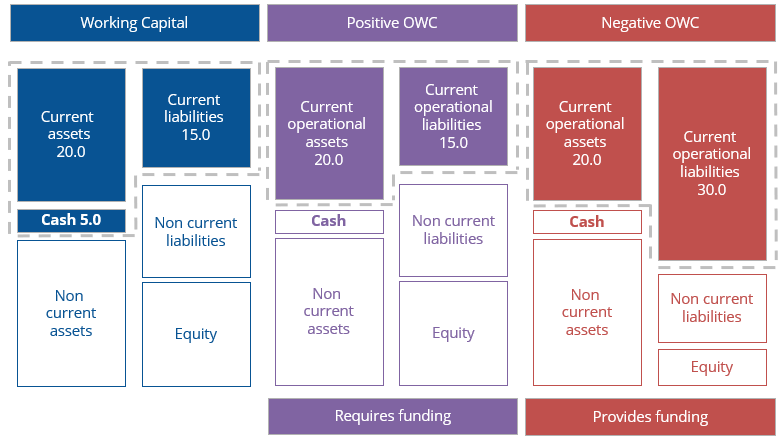

Operating working capital is defined as operating current assets less operating current liabilities. Operating represents assets or liabilities which are used in the day-to-day operations of the business or if they are not interest-bearing (financial). Cash and other financial assets are typically excluded from operating current assets and debt is normally excluded from operating current liabilities.

Operating Working Capital (OWC) = Operating Current Assets – Operating Current Liabilities

Key Learning Points

- Working capital is a measure of liquidity and is calculated as current assets less current liabilities

- Operating working capital focuses on the operating short term assets and liabilities required to run a business’s operations and is calculated as operating current assets less operating current liabilities

- Positive OWC indicates cash is tied up in the business’s operations, and short-term funding is required. Negative OWC implies that the company has access to a “free” source of short term funding.

- Although negative OWC is a useful source of cash it may not be appropriate for all businesses. There’s no one ‘right’ OWC level. It depends on the industry.

Cash flow is fundamental for successful businesses and not having cash readily available could result in a loss of opportunities and failure to meet financial obligations. Working capital is current assets less current liabilities and is often expressed as a percentage of sales in order to compare businesses within a sector. The measure attempts to assess the short-term liquidity of a business and determine how well the company can cover the payment of its forthcoming liabilities. It provides an indication of how much cash a business has tied up in current assets and whether it can cover its short-term obligations.

If an industry has inventory that cannot be easily liquidated then often an amended version of the metric is calculated. This uses current assets less inventory instead of current assets and is called the acid test or quick ratio.

Operational Assets

Operational assets are resources used to generate revenues and, therefore, essential for ongoing business operations. Inventories accounts receivable, and prepaid assets are all examples of short-term operational assets. Cash is often excluded as it is seen as a financing item, with its level seen as a choice rather than a necessity to run the business. However, sometimes it may be operational if a business requires cash to operate, such as a travel shop for currency exchange.

Operational Liabilities

Operational liabilities are classified as non-interest-bearing liabilities and result from the operational activities of the business. Accounts payable, salaries payable, and most accrued liabilities are all operational. They are not interest-bearing (in the normal course of business) and, therefore, often referred to as providing “free funding” to the business.

Understanding Operating Working Capital

A business with positive OWC, where short-term operating assets are greater than short-term operating liabilities, requires short-term funding. Cash is “tied up” in the company creating the funding requirement. Businesses with negative OWC, where short-term operating liabilities are greater than short-term operating assets, get extra “free funding”.

Think of a dominant supermarket in your area. In the UK it was Tesco for a long time. Tesco has extraordinary power over its suppliers. It’s such a big buyer and its suppliers are small in comparison. Tesco can demand very generous credit terms from farmers and other suppliers, meanwhile demanding cash from its customers in-store. You can’t buy a loaf of bread on credit. This means big supermarkets often have negative OWC balances, and are using their suppliers as ‘free finance.

Problems with OWC?

You need to be careful when using OWC as an operational measure, as it is very dependent on the industry and how the company operates. Many analysts use the metric to compare two or more businesses of different sizes by representing the number as a percentage of sales. This makes the metric more comparable as the absolute number calculated before only provides just that, a number. The larger the business, the larger the number due to the scale of their operations rather than their efficiency. It is meaningless to compare companies of different sectors due to the difference in the characteristics of the industry.

Example Operating Working Capital

Operating working capital is calculated using numbers obtained from the balance sheet. Normally, the analyst would also use some footnote details to ensure that the current assets or liabilities in question are truly operational in nature.

The balance sheet numbers for AM Kensington Ltd. are given below. Download the accompanying Excel files to practice calculating operating working capital using these numbers. You can learn more about working capital with The Accountant course