Test Yourself

Sign up to access your free download and get new article notifications, exclusive offers and more.

Equity Forwards

June 22, 2022

What are “Equity Forwards”?

Equity forwards are customized contracts between two counterparties who agree to buy or sell a stock at a specified price on a future date. The future date is the expiry date of the equity forward contract. The forward price (predetermined delivery price) is locked in with the forward contract, and the contract is obligatory. Forward contracts are traded over-the-counter and settled on expiration.

Equity forwards have terms that range from one day to several years and are used to hedge price risk in a stock or a stock portfolio. Forwards can also be used as investment instruments to profit from anticipated price movements. Equity forwards can be used to speculate on future movements of stock indices or individual stocks. Equity forward contracts are cash settlements, with no cash changing hands until contract expiration. Forward contracts are derivative instruments since their value is “derived” from the underlying asset. Moreover, such a type of contract derives its value from the underlying assets.

Key Learning Points

- Three key terms are important in understanding equity forwards – underlying assets, long and short sides of the contract, and forward appreciation and depreciation.

- In an equity forward contract, the price and quantity (size) of the underlying asset to be traded are known at the initiation of the contract. However, the unknown is the price at contract expiration.

- The forward price is determined by one of three formulas, depending upon the circumstances. The first calculates price without carrying costs, the second with carrying costs included, and the third is used when dividends are paid on the stock.

Equity Forwards – Terminology and Risks

Underlying asset is the stock or stock index upon which the contract is based.

Long side and short side: The counterparty that has agreed to purchase the underlying asset on some specified future date is said to be on the long side of the contract. The counterparty that has agreed to sell the underlying asset at the strike price on the specified date is on the short side of the contract.

The long side of the contract is obligated to purchase the underlying asset at the forward price on the contract expiration date. The short side of the contract is obligated to deliver the underlying asset on this date at the forward price.

Equity forward appreciation and depreciation: suppose the current market price of the underlying asset, for example, the current price of a specific stock, appreciates (depreciates), then the value of the long side also appreciates (depreciates). Conversely, if the current market price of the underlying asset appreciates (depreciates), the value of the short side will depreciate (appreciate).

The forward price is based on several factors including the spot (current) price of the underlying asset and costs such as interest rates, foregone interest, or opportunity costs.

In an equity forward contract, the price and quantity (size) of the underlying asset to be traded are known. However, the spot price on the delivery date is not.

Equity forward transactions carry several types of risk exposure. First, there is the risk that the forward price will be unfavorable at the spot price on the settlement date.

For example, on the short side a seller has agreed to deliver an underlying asset at the strike price. If the forward price is lower than the spot price on the exercise date, the seller will suffer a loss in the amount of the spot price minus the forward price. If the forward price is higher than the spot price, the seller will profit by the difference between the forward price and the spot price.

On the long side of the contract, if the spot price at expiration is higher than the forward price, the buyer will profit by the difference between the forward price and the spot price. Likewise, if the spot price is lower than the forward price, the buyer will lose money. It is important to remember that in a cash settlement contract, one of the counterparties will pay the difference between the spot and forward to the other. No physical delivery will be made.

Another risk relevant to forward contracts is default risk. Each counterparty is exposed to the risk of default, which occurs when one counterparty fails to satisfy the terms of the contract. Equity forward contracts carry credit risk and are also subject to liquidity risk.

It’s also important to take into account the impact of leverage, which is the difference between the amount pledged as margin and the underlying value of the equity contract. The margin component enhances the risk of loss when trading equity forwards on margin.

Equity Forwards – Illustration

Suppose that a client has entered into an equity forward contract with a bank. The client (long side) agrees to buy 400 shares of a publicly listed company for US$ 100 per share from the bank (short side) on a specified expiration date one year in the future.

Now, If the underlying asset price (the stock price) rises to US$ 150 dollars on the settlement date, the long side of the forward contract will make a profit. The long side of the contract would only have to pay the forward price of US$ 100 dollars to take delivery of this stock that is worth USD 150 per stock – making a gain of US$ 50 per share. However, if the stock price falls to USD 80 per share, the long side would still be obligated to buy the stock at US$ 100 per share, for a USD 20/share loss. forward price to take delivery of the stock even though the stock was only worth USD 80.

On the short side of the contract, if the stock price rises to USD 150, the bank has to deliver the 400 underlying shares selling at the current price but will receive only US$ 100 per share. Therefore, the bank will suffer a loss of US$ 50 per share. However, if the underlying price of the stock falls to USD 80, the bank would have to deliver the but would receive USD 100 dollars per share, resulting in a USD 20 per share gain.

Equity Forwards – Pricing

There are several factors that influence the price of a forward contract, the most important being the price of the underlying asset. Price fluctuations of equity forward contracts are chiefly driven by changes in the price of the underlying stock.

The money market rate also influences pricing. A high (low) money market rate will result in a high (low) premium on such contracts. Equity forwards are an alternative to purchasing the underlying asset. Dividends paid during the term of the contract are another important influence on pricing.

Formula

The forward price is determined by the following formula:

F = SP * e^(r*t)

F= the forward price of the contract

SP = the current spot price of the underlying asset (stock or stock index)

R = risk-free rate applicable to the term of the equity forward contract

T = the settlement date in years (for example, one year)

E = mathematical irrational constant approximated by 2.7183.

If there are carrying costs, then the formula changes to:

F = SP * e^(r+m)*t

M = the carrying costs, such as interest, storage costs, or opportunity costs.

If the stock (underlying asset) pays a dividend over the term of the contract, the formula to compute the forward price changes to:

F = (SP – D) * e^(r+q)*t

D = sum of each dividend’s present value (PV) i.e. D = PV (D(1)) + PV (D(2)) + …. PV (D(n))

Suppose an equity forward contract expires in one year, and the underlying asset pays a 20-cent dividend every three months. Then we have D = PV (D(1)) + PV (D(2)) +PV (D(3)) + PV(D(4)).

Equity Forwards – Example

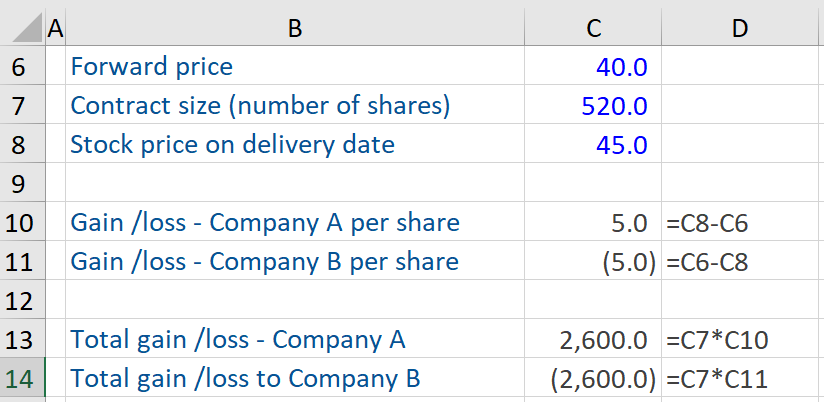

Company A and Company B are counterparties to an equity forward contract. The underlying asset is the stock of a blue-chip company (Z) and the size of the contract is 520 shares. Company A is the long side of the contract and Company B is the short side of the contract.

The forward price, contract size, and stock price on the delivery date are given. Based on this information, determine the gain or loss per share and total gain or loss for both the counterparties.

Look at the difference between the forward price and the spot price on the delivery date. Company A will purchase the stock on the delivery date and will make a gain (per share) if the stock price is higher than the forward price. Company B will make a loss per share as the spot price is higher than the forward price on that delivery date. Company B will receive 40 per share, while the market price on the delivery date is 45.

To determine the overall gain or loss for both counterparties, we multiply the gain or loss per share by the size of the contract or 520 shares. The total gain for Company A is 2,600 and the total loss for Company B is 2,600.