Mezzanine Warrants

What are Mezzanine Warrants?

Mezzanine warrants are equity participation rights that are attached to a junior, subordinated loan within a highly leveraged capital structure. The purpose of the warrants is to enhance the return to the mezzanine lenders for making such a risky loan.

Key Learning Points

- Mezzanine warrants are often called “equity kickers” as they can provide a positive jolt to the return if the deal is successful. If the deal is not successful, they do not need to be exercised.

- The ownership percentage attributed to the warrant will vary depending on the lender’s required return, the risk and projected growth of the business, and other factors but generally falls between 1% and 5%

- Warrants are technically securities and can be exercised or transferred. However, it is uncommon for transfers to happen in the private equity context due to outside owner concerns

- There are several ways to structure a warrant to transfer ownership including offering a certain number of shares, percentage ownership, equity contribution, and debt conversion

- Most mezzanine investors are not seeking to become long term equity investors but rather to enhance yield on the loan

The Use of Mezzanine Warrants

Since mezzanine lenders sit in a very vulnerable place in the capital structure, they are always seeking ways to enhance return at no additional cost. The return to mezzanine investors consists of three components:

1) Fees (the commitment fee, which is often OID, as well as prepayment fees)

2) The coupon (this can be cash or PIK or both

3) Equity participation

The warrants that are attached to the mezzanine debt provide that the institutional owners of the common equity will transfer a percentage of ownership to the mezzanine lenders upon exercise, typically at a pre-agreed upon event such as sale or IPO.

Types of Warrants

There are several types of warrants:

- Right to purchase a specified number of shares – this is usually less desirable due to potential dilution from options

- Right to purchase a percentage of equity -this is the most common and usually triggered by an event such as a recap, sale of issuer, refinancing, or IPO

- Right to co-invest alongside institutions – this is more common for equity-focused mezzanine funds, credit focused funds tend to avoid this

- Put option to convert the debt to equity – this is less common

Valuing the Warrants

While warrants are technically securities and can be valued, most are considered valueless until a specified event transpires. Transferring ownership is not generally allowed as private equity sponsors of closely held companies are not seeking new outside owners who have not been vetted.

The warrants will provide value at one of the predefined events when the value of the company can be ascertained. At the time of sale or IPO, the equity is re-valued. For recaps or refinancings, the valuation of the equity is more challenging.

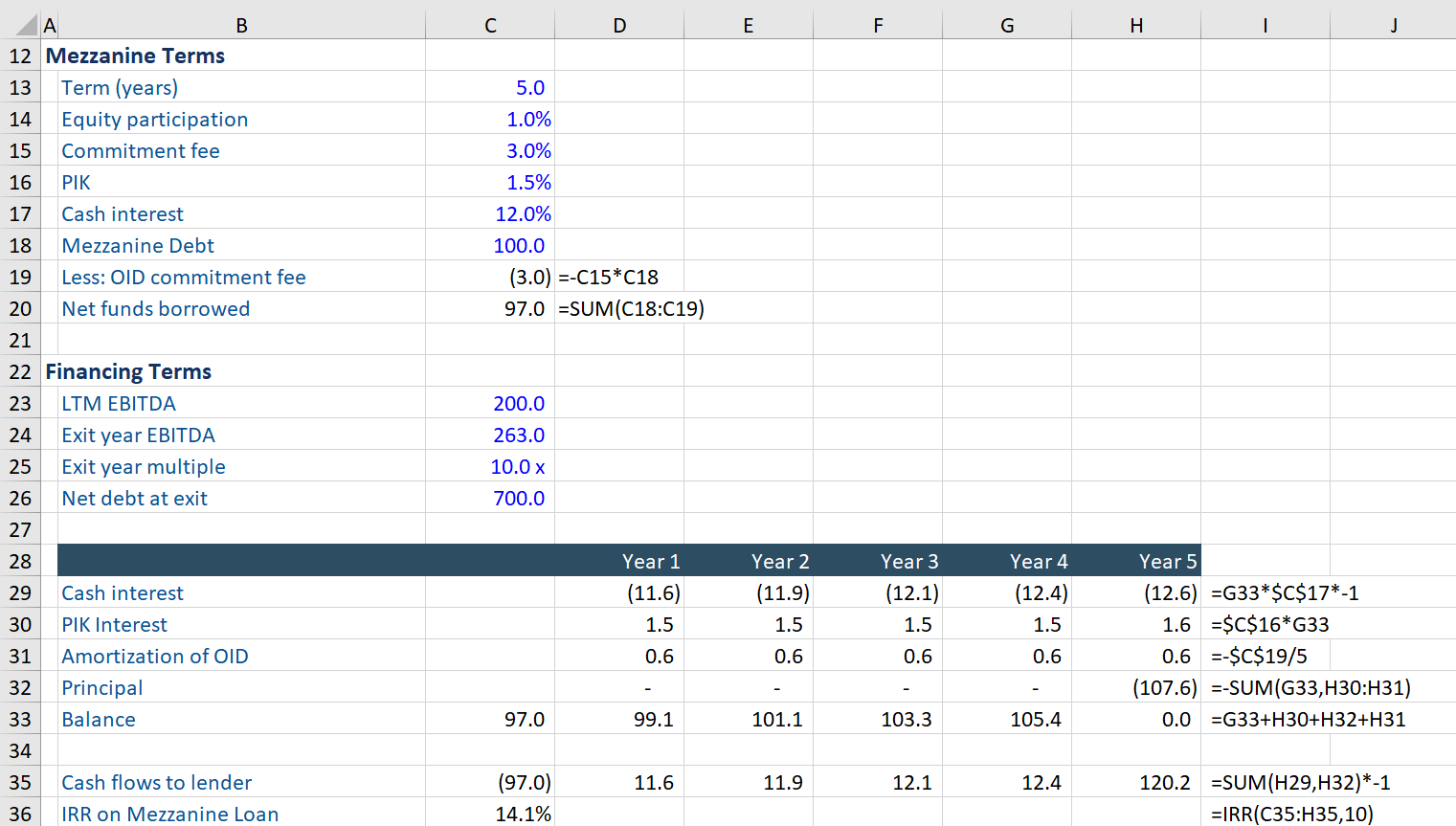

The calculation of the return to the mezzanine holders begins with the IRR of the cash flows received from the issuance of the debt up to the repayment at the event. This will consist primarily of the fees, cash interest, and accrual of value via the PIK interest. In the example below, the return on the debt alone is 14.1%.

At that event, the mezzanine warrant holder can also participate in the upside of the equity growth according to the percentage of ownership defined in the warrant, in this example, 1.0%.

We can see that the incremental return offered by the warrants versus the loan without participation is over 300 basis points at 16.8% due to the success of the deal.

Conclusion

Mezzanine warrants are a feature of mezzanine debt that can enhance the yield to the lender. By acquiring equity participation rights, the lenders can, at no cost, share in the upside of a deal which helps mitigate the riskiness of lending lower in the capital structure. Learn more about mezzanine financing with our online private equity course.